- Boundless Discovery

- Posts

- India–Pakistan: A War the World Can't Afford

India–Pakistan: A War the World Can't Afford

Harry Lyons

June 04, 2025

This week, Boundless Discovery examines a conflict risk that rarely appears in global forecasting models but should: the India–Pakistan standoff. The world already knows that a crisis in the Taiwan Strait would paralyze the global semiconductor supply chain. It watches China’s grip on rare earth elements with unease, knowing they power everything from electric vehicles to defence systems. It tracks tensions in the Strait of Hormuz, where a single missile strike could spike global oil prices overnight. But few ask the same of South Asia: what happens if a war breaks out between India and Pakistan?

The answer lies deep in the wiring of the global economy. What makes their rivalry uniquely significant today isn’t just the nuclear dimension—it’s how deeply both countries are now embedded in global supply chains and services.

Though the territorial dispute over Kashmir has persisted since partition in 1947, the global stakes have transformed. The recent four-day military escalation brought both countries to high nuclear alert and drew widespread diplomatic interventions from Washington, Beijing, Tehran, and Riyadh. As the world economy grows increasingly dependent on South Asian stability, understanding this conflict's global ramifications has never been more important.

At Boundless, we research geopolitics, technology, and the global economy using the same software we deploy to help businesses navigate their external environment. We map your ecosystem—customers, competitors, suppliers, and regulators—to reveal hidden opportunities before they become costly.

See where you’re exposed. Know where you have leverage. Turn intelligence into strategic and financial advantage.

Contact us here to map your market—and take control of the terrain.

You can read this in our interactive platform here! (Note: It's not mobile-friendly yet, so if you're on your phone, just keep reading below.)

Explore our comprehensive event graph below—packed with insights too rich and interconnected to capture in words alone.

CRITICAL CONTEXT: A BRIEF HISTORY OF THE KASHMIR CONFLICT

The Kashmir dispute has transformed over decades—from a crisis of post-colonial statehood into a nuclear-anchored fault line. Each phase hardened the conflict and added a new layer of complexity to an already volatile geopolitical standoff.

Partition's Broken Blueprint: In 1947, British withdrawal from India and the subsequent partition of the country into two independent nations—India and Pakistan—was executed with impossible speed. British lawyer Cyril Radcliffe, who had never visited the region, was given just five weeks to draw new borders, splitting Punjab and Bengal, which both contained roughly equal Muslim and Hindu populations. The result: the largest mass migration in human history—14 million displaced and between 500,000 and 2 million killed.

(Map of the partition of India (1947) source: Wikipedia)

Kashmir’s Dilemma: Kashmir, one of 565 semi-autonomous kingdoms given the choice to join either India or Pakistan, faced a unique dilemma. Its Hindu ruler governed a majority-Muslim population. In October 1947, Pakistani-backed militias invaded. India intervened militarily as soon as Kashmir’s ruler, Maharaja Hari, formally acceded to the Indian Union.

The First Kashmir War (1947-1949): The first Indo-Pakistani war followed immediately. Indian and Pakistani forces clashed across the region, with control of Kashmir hanging in the balance. The UN-brokered Karachi Agreement in January 1949 established a ceasefire line which would later go on to be officially recognised as the Line of Control (LoC) in the wake of the 1971 Indo-Pakistani War. This line remains the de facto border today.

(The disputed area of Kashmir, Source: United States Central Intelligence Agency)

Second Kashmir War (1965): Pakistan launched Operation Gibraltar, attempting to incite a popular uprising in Indian-administered Kashmir by infiltrating militants. Instead, it triggered a 17-day conventional war which was the largest armoured conflict since World War II. The war ended in a ceasefire under pressure from U.S. and Soviet diplomacy, with no significant change in territorial control.

Nuclear Nations (1998): In May 1998, both nations crossed the nuclear threshold within weeks of each other. India conducted Operation Shakti on May 11, becoming the sixth declared nuclear weapons state. Pakistan responded with Chagai-I and Chagai-II tests on May 28, becoming the seventh nuclear power. These tests fundamentally altered the strategic dynamics of the Kashmir dispute, with both sides now operating under the shadow of potential nuclear escalation.

Kargil Conflict (1999): Pakistani forces secretly occupied strategic heights on the Indian side of the Line of Control during winter, hoping to present India with a fait accompli. Two months of intense mountain warfare saw India slowly recapture most infiltrated positions, while international pressure—particularly from Washington concerned about nuclear escalation—compelled Pakistan's withdrawal.

Proxy Warfare Era (2001-2016): Nuclear deterrence shifted conflict toward proxy warfare, with attacks like the 2001 Indian Parliament assault and 2008 Mumbai attacks bringing the countries to the brink of larger war while avoiding major military exchanges.

Controlled Retaliation (2016-present): Modern incidents such as India's 2016 "surgical strikes" and the 2019 Balakot airstrikes have established a pattern of precise, limited retaliation designed to signal resolve while avoiding catastrophic miscalculation in a nuclear context.

2025: THE PAHALGAM CATALYST

Trigger Event: On April 22, Twenty-six civilians, mostly Hindu tourists, were killed in a mass shooting near Pahalgam in Jammu and Kashmir. The Resistance Front (TRF), an offshoot of Pakistan-based terror organisation Lashkar-e-Taiba, initially claimed responsibility before retracting the claim. Indian authorities identified an ex-Pakistan Army Special Forces soldier as the prime suspect, citing this as evidence of official Pakistani involvement.

Operation Sindoor: On May 7, 2025, India launched 14 coordinated strikes across 23 minutes, targeting nine locations in Pakistani-administered Kashmir and Pakistan's Punjab province. India described the strikes as "focused, measured, and non-escalatory," claiming they targeted the infrastructure of the terror groups Jaish-e-Mohammed and Lashkar-e-Taiba without hitting Pakistani military facilities.

Pakistani Retaliation and Ceasefire: Pakistan responded with missile strikes, drone attacks, and artillery shelling along the border that struck Kashmir and beyond. The four-day conflict marked the most serious escalation since the 2019 Balakot crisis. A ceasefire was announced on May 10 following hotline communication between military commanders.

Global Stakes Drive Universal Intervention: Countries including the US, China, Russia, UK, Saudi Arabia and Iran all directly engaged in de-escalation efforts, with US officials making direct calls to Indian and Pakistani leaders on May 9. The diplomatic engagement from Washington to Tehran and Beijing demonstrated how a conflict between these major powers quickly draws global intervention regardless of traditional alignments.

An Underrecognized Flashpoint: The escalation lasted only four days, but its reverberations echoed around the world and unveiled a lesser-appreciated vulnerability in the international system. While geopolitical risk assessments typically focus on US-China tensions or Russian aggression, the India-Pakistan standoff represents an under-analysed threat—two nuclear powers so embedded in critical global supply chains that sustained conflict would trigger global disruption on an unprecedented scale.

CRITICAL DEPENDENCIES: WHERE THE WORLD HINGES ON INDIA

India's transformation from a developing economy to a vital node in global supply chains has happened largely below the radar of international risk assessment. Today, the country functions as an irreplaceable supplier across multiple essential sectors that would face immediate disruption in any sustained conflict scenario.

Indian Pharmaceuticals – The Affordable Global Pharmacy

ndia is the backbone of the global generic pharmaceutical supply. Its industrial-scale manufacturing and regulatory compliance have made it the preferred supplier for much of the Global South and the silent workhorse behind Western health systems.

Volume Over Value: Despite ranking 11th globally for pharmaceutical exports by export value, shifting the metric from value to volume reveals the true significance of India to the integrity of the pharmaceutical market – India places 3rd by volume accounting for 20% of all global generic exports. This includes:

40% of U.S. generic drugs

25% of all UK medicines

60% of global vaccine output

80% of AIDS antiretrovirals used in Africa, Asia, and Latin America

50% of Africa's generics

What breaks if it falters: Hospital pharmacies stall, global vaccination drives falter, NGO relief efforts collapse, and the world's most vulnerable populations lose access to affordable treatment.

Time to pain: Weeks. Critical national and NGO stockpiles begin depletion within two weeks, especially for critical antibiotics and antiretrovirals.

Who feels it: All Western healthcare systems across North America and Europe, African public health programs, humanitarian logistics arms of WHO, UNICEF, Medecins Sans Frontieres, and Global Alliance for Vaccines and Immunization.

Replacing Supply: Very difficult. China lacks sufficient FDA-approved facilities and export reliability. Western producers face prohibitive cost and time-to-scale barriers. India operates 10,000+ pharma facilities and 650+ U.S. FDA–approved plants, making it irreplaceable in volume-driven drug pipelines.

India doesn't just make medicine. It props up the entire model of affordable, scalable healthcare for most of the planet.

INDIA'S ROLE IN THE DIGITAL SUPPLY CHAIN: POWERING THE BACKEND OF GLOBAL BUSINESS

India is the global epicentre of outsourced IT and business process outsourcing (BPO) services. From cloud architecture to financial reconciliation, it quietly keeps the modern economy running.

$254 Billion Sector: In 2024, India's IT and Business Process Outsourcing (BPO) industry generated $254 billion in revenue, including $50+ billion in exports to the U.S. India is more than an outsourcing hub, it has become uptime insurance.

Powered by People: Over 5 million professionals support this sector. Indian firms also directly employ 1 million Americans, with core delivery hubs in Bangalore, Hyderabad, Pune, Chennai, and Gurugram.

Near-Universal Dependence: 75% of U.S. firms and 80% of European firms outsource IT or BPO functions to India with most Fortune 500s maintaining significant tech hubs in-country.

What Breaks if it's Disrupted: If India’s IT and BPO backbone goes offline, the ripple effects hit fast. Call centres go dark. Payments stall. Cloud systems falter. Across industries, everything from customer support to backend operations begins to fail—revealing how much of the global economy silently runs on Indian code and manpower.

Time to Pain: 48–72 hours. Real-time dependencies mean failures cascade fast.

Who Feels It: The global outsourcing ecosystem would be hit hardest, with industry giants like Accenture (employing over 300,000 people in India) and IBM (over 140,000) particularly exposed. Tech leaders such as Amazon (100,000), Microsoft (over 20,000), and Google (10,000–15,000) would also face major operational disruptions, highlighting just how deeply these companies rely on India’s talent pool and cheap labour for their global operations.

Replacing Supply: Very difficult. No other geography matches India's scale, skill density, time-zone flexibility, and cost ratio. Alternatives like Poland, Vietnam, and the Philippines lack capacity and depth in key functions.

RICE: THE SOUTH ASIAN STAPLE THAT FEEDS THE WORLD

Rice is the backbone of global food security—and no country moves more of it than India. Together with Pakistan, they supply over half the world's traded rice, feeding billions with this staple of the human diet.

South Asia’s Rice Dominance: India and Pakistan together account for over 50% of global rice exports, forming the central artery of global rice supply.

India: Rice exports are projected to reach ~24 million metric tons (MMT) in 2025–26. This is roughly 40% of global trade, according to the U.S. Department of Agriculture.

Pakistan: The fourth-largest rice exporter globally, is expected to contribute ~5.8–6.0 MMT in 2025–26. This accounts for approximately 10% of the global export market.

What breaks if Indian rice exports are disrupted: Food inflation and rationing across dozens of food-insecure countries. The UN’s World Food Programme scrambles to source calories elsewhere and nations who are heavily reliant on India for rice imports face rapid depletion.

Who Feels It: This 30 MMT supply chain underpins food security in regions like Africa (e.g. Somalia sources over 80% of its rice from India), the Middle East (Saudi Arabia and Iran, rely on India for over 80% and 95% of imports respectively), and Asia (e.g. Bhutan and Nepal, both import over 95% of their rice from their neighbour), while also sustaining global humanitarian pipelines like the World Food Programme.

Replacing Supply: Very difficult in the short term. Thailand and Vietnam cannot immediately replace the ~30 MMT combined capacity. Even in the wake of a partial export ban by India in 2022-2023, global rice prices rose 15–25%.

PAKISTAN’S POSITION IN GLOBAL SUPPLY CHAINS

Pakistan's role in global supply chains appears more modest than India's, but the country occupies strategic choke points that amplify its economic importance far beyond its GDP. Beyond the global rice trade, the country sits at the crossroads of critical supply chains—exporting the medical tools that enable surgery, the textiles that fuel the fashion industry, and enabling infrastructure vital to China’s westward ambitions. Its contributions are often under-recognized, yet their disruption would be felt far beyond South Asia.

SIALKOT'S SURGICAL SUPPLY CHAIN

On the edge of Kashmir, the city of Sialkot powers a critical slice of global healthcare. Each year, it produces over 150 million surgical and dental tools—more than 95% of which are exported. Though its name rarely appears on packaging, Sialkot-built instruments are used daily in hospitals across Europe, the U.S., and beyond. Its disruption would delay surgeries and disrupt aid missions worldwide.

Unseen, Ubiquitous, Irreplaceable: Sialkot, is the world's core supplier of white-label affordable surgical hardware. It produces an estimated 25% of all handheld surgical instruments, with some industry sources suggesting that this figure rises to 70% for certain equipment. In 2018, 80–90% of all surgical tools purchased by the NHS Supply Chain were made in Sialkot.

What breaks if it's disrupted: Elective and emergency surgeries are cancelled as hospitals run short of forceps, clamps, and scissors. Humanitarian missions stall: Médecins Sans Frontières and Red Cross clinics in crisis zones lack basic kits. Procurement programs in the UK’s NHS and EU health systems scramble for costlier alternatives with longer lead times.

Time to pain: Weeks. As evidenced by the COVID-19 pandemic, hospital and NGO stockrooms empty fast and typically do not stockpile supplies.

Who feels it: UK, EU, and U.S. public health systems. Aid networks in Africa, South Asia, and conflict zones. Global brands that source instruments from original equipment manufacturers in Sialkot, often under white-label arrangements.

Replacing Supply: Very difficult in the short term. Other major producers like China and Germany cannot match Sialkot's speed, scale, or cost-performance ratio. Building a new supply base takes months at best and surgeries stall as soon as cheap clamps and forceps run out. Sialkot is not just a low-cost convenience, it's a critical node in global surgical continuity.

BEYOND THE LABEL: PAKISTAN’S TEXTILES AND THE GLOBAL CLOTHING ECONOMY

Pakistan is the world's seventh-largest textile exporter and the fourth-largest cotton producer. It runs one of the most vertically integrated textile ecosystems on the planet—spinning, weaving, dyeing, and stitching all happen in-country. The industry accounts for 60% of the country's exports, employs 25% of the national workforce, and operates over 50,000 production units.

What Breaks If It's Disrupted: Global brands lose core product lines: Nike and Adidas face sportswear shortages; Levi's and Tommy Hilfiger lose denim production; Walmart, Target, and Macy's run low on home textiles. Fast-fashion chains (Zara, H&M) lose seasonal inventory.

Time to Pain: 4–6 weeks. Most buyers operate lean, just-in-time pipelines.

Who Feels It: Major apparel brands (Nike, Adidas, Levi's), U.S. retailers (Walmart, Target, Bed Bath & Beyond), European fast-fashion chains, and emerging direct-to-consumer brands.

Replacing Supply: Moderate difficulty. Bangladesh and Vietnam can cover some output but not towels, denim, and cotton yarn at Pakistan's cost and speed. Global buyers face higher prices, slower shipping, and product gaps.

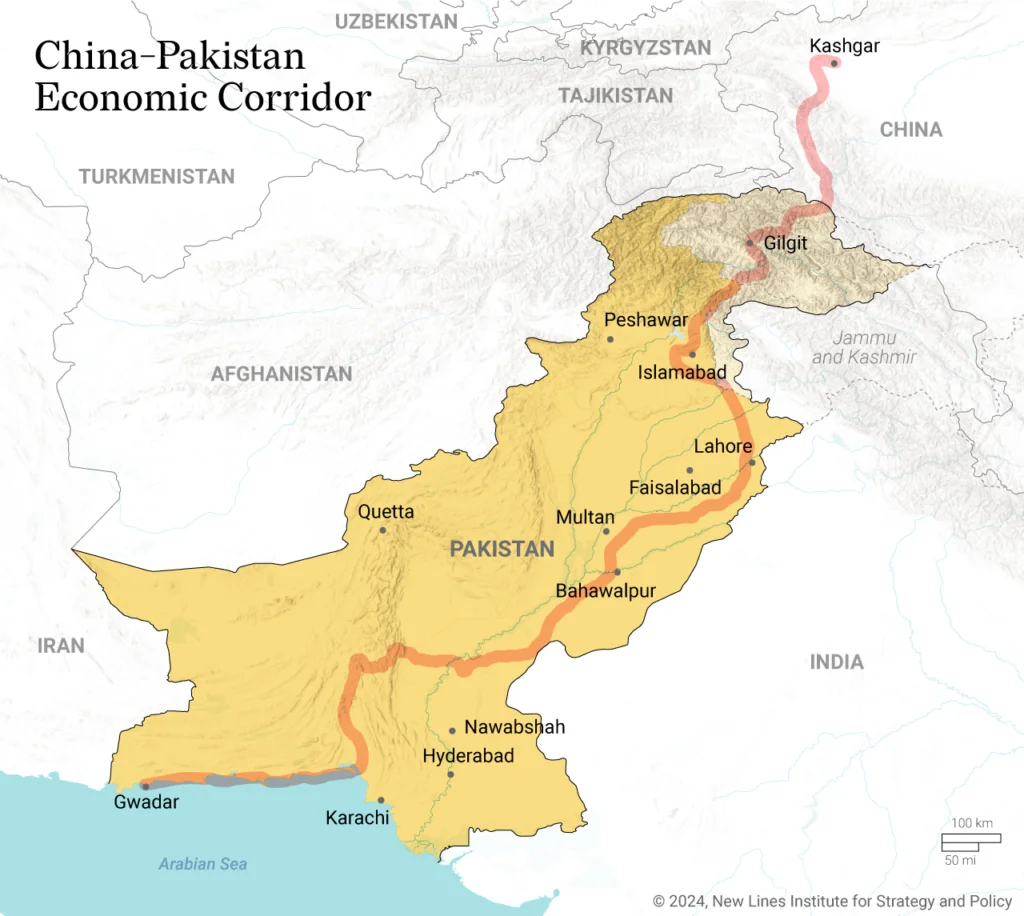

THE CHINA–PAKISTAN ECONOMIC CORRIDOR (CPEC)

The CPEC is the flagship corridor of China's Belt and Road Initiative (BRI), designed to provide Beijing direct overland access to the Arabian Sea. China has thus far pledged $62 billion of investment to develop this trade corridor which bypasses chokepoints like the Strait of Malacca and U.S.-influenced routes. Its critical components include:

Highways & Rail: The 3,000 km highway and rail network connecting Kashgar (Xinjiang) to Gwadar Port in Balochistan. Key arteries include the Karakoram Highway, the ML-1 railway upgrade, and the Hazara Motorway.

Energy Infrastructure: Coal, hydro, solar, and LNG power projects across Pakistan, supplying ~10,000 MW in added capacity. Power plants like Sahiwal and Port Qasim are joint ventures backed by Chinese state firms.

Fiber Optic Cables: The 820-km cross-border China–Pakistan Fiber Optic Cable links Rawalpindi to Khunjerab Pass and onward to China, forming part of the Digital Silk Road.

Gwadar Port: A deep-sea port leased to China Overseas Port Holding Company. Once billed as the "next Shenzhen," investment in Gwadar is intended to elevate it to the level of Dubai as a logistics and trade hub.

(The China-Pakistan Economic Corridor: 3,000km route connecting Kashgar in China's Xinjiang province to Gwadar Port, source: New Lines Institute for Strategy and Policy)

If War Breaks Out the CPEC runs through the heart of the escalation zone:

Gilgit-Baltistan: A region claimed by India but administered by Pakistan, serves as the critical mountain entry point for CPEC

Balochistan: The home of the Gwadar Port, has a long-running insurgency and would become a prime target in any India-Pakistan confrontation.

A sustained conflict would threaten the entire China-Pakistan Economic Corridor, an initiative already strained by debt concerns and implementation delays. Critical infrastructure including Gwadar port, energy pipelines, and digital networks would face operational disruptions, undermining years of Chinese investment and strategic planning. The economic paralysis would likely force Beijing to wholly reconsider the viability of the Belt and Road project in South Asia.

Why It Matters Globally:

China's Energy and Trade Insurance Policy Dies: The CPEC was meant to secure Beijing's access to Middle East oil and African minerals independent of U.S. naval chokepoints. A war renders that corridor unreliable, pushing China back to vulnerable maritime dependence

Ripple Effect Across BRI: From mining sites in Africa to industrial parks in Central Asia, many Chinese-led projects rely on stable east-west movement through Pakistan. A shutdown or re-routing forces delays, higher costs, and re-exposure to maritime corridors.

Replaceable? No. While China is actively pursuing alternative westward routes—via Afghanistan, Iran, and the China–Kyrgyzstan–Uzbekistan corridor—none offer immediate or scalable alternatives to CPEC. The Afghan option remains highly unstable, Iran is sanctioned, Myanmar is embroiled in conflict, and many Arctic routes are still years away from viability.

History suggests that India and Pakistan will fight again. The May flare-up saw airport closures, flight rerouting around Pakistani airspace, and severe volatility in both countries' stock exchanges—but a sustained conflict would go far beyond transport disruption and market speculation.

Critical supply chains would be at risk, and the numbers reveal why: 80% of AIDS drugs in Africa, 40% of American generics, 75% of Fortune 500 IT operations, 50% of global rice exports, and one Pakistani city controlling surgical instrument supply worldwide. These statistics represent single points of failure in a system that assumes perpetual stability between historical adversaries.

Reply